SaaS founders lose.

Summary

In today's world of SaaS…

Customers win: they are better off because they don't pay upfront

Businesses win: more profitable in the long run

VCs win: they profit from the financing

Founders lose: from more dilution

Software Era of 2000s

Back in the day, after a software company develops the product (R&D), each unit of software they sell is strictly profitable from day 1.

In essence, customers cover the acquisition cost upfront. As a result, as a growing company, you need to figure out how to finance the cost of R&D. This can either be done via the different traditional means: equity, debt or from cash flow.

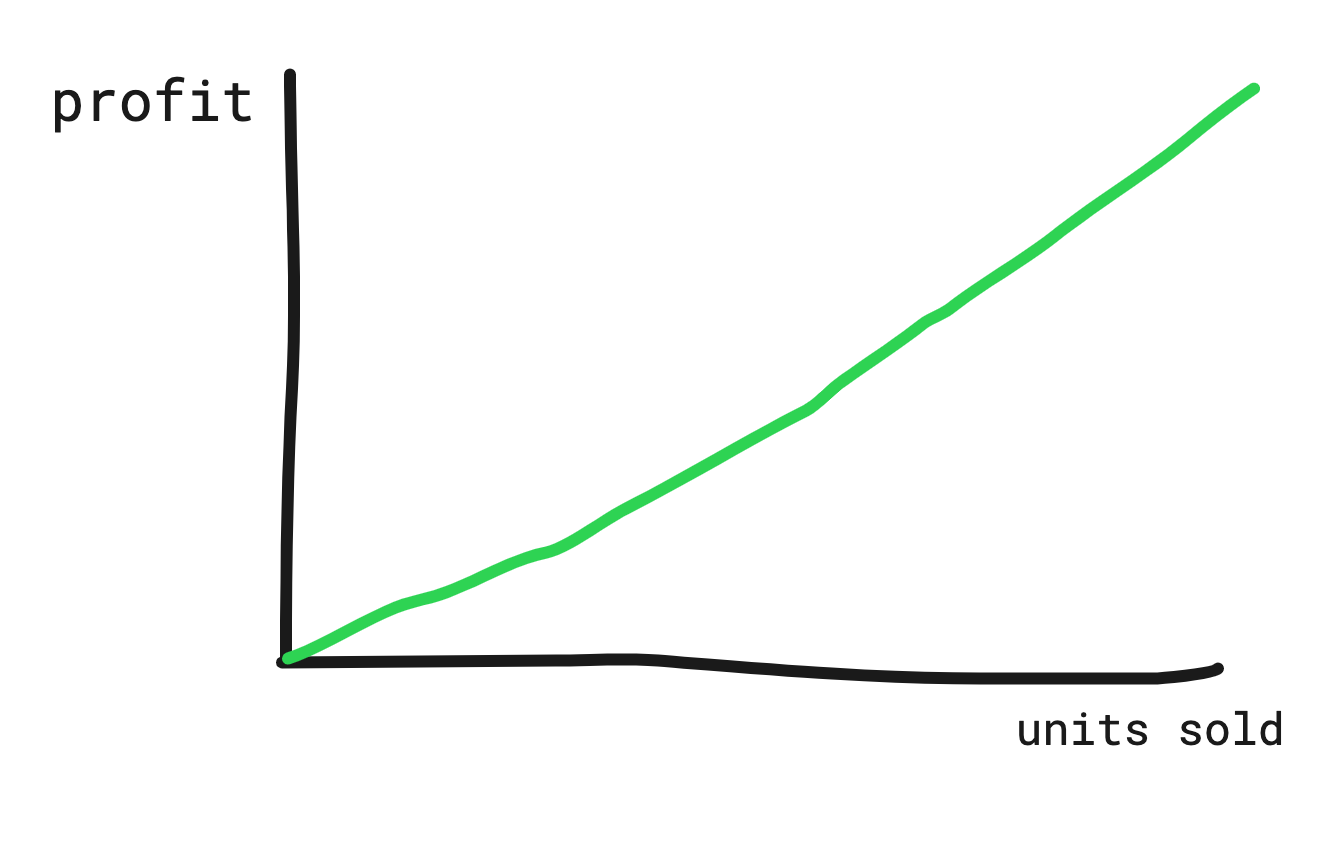

For example: aside from the cost of developing the software, once that's done, for an acquisition cost of $90, you would sell the product for $100.

Take a CD software like Microsoft Office for example. You raise capital to build the software (R&D) and then you sell discs of CD going forward.

If we were to graph your revenue curve, it looks something like this:

For every unit you sell, you make $10 in our example. Sell 100 units, make $1,000. Now you need to make sure you are selling enough units to cover your cost of R&D or fixed costs, but from a growth perspective, you're making contributions towards that gap from day 1 of sales.

Whatever the software is worth to you from a fully loaded acquisition perspective, you had to make sure that the customer paid you that full amount plus more (which is your profit & contribution margin) on day 1, or else your business has negative unit economics.

The new world of SaaS

"Software as a service" was a new terminology that was pioneered in the early 2000s, Salesforce being one of the first to popularize the concept.

From a customer perspective, SaaS eats traditional software's lunch, and this is because it's a better customer experience, where they don't need to pay for the whole software upfront, instead they pay as they derive value from the product.

Similar to car leasing, the company is now financing the customer to use their product, with hopes that the value is there and they will continue to use it. Practically there are two outcomes here for the business:

LTV is higher because the customers who do derive value from the product will use it for much longer and therefore pay for that value.

CAC is lower because the barrier to entry is now lower and net out better funnel conversion rates than their traditional software counterparts.

In our earlier example of selling the CD software for $100, now we don't charge $100, but rather we charge $10 per month. For the sake of simplicity, let's say it still costs $90 to acquire the customer, but because we charge $10/month and expect to retain the customer for 12 months, the effective LTV is now higher ($10 * 12 months = $120 LTV)

However, from a cash flow perspective, the company also doesn't receive the revenue upfront, instead it's spread across 12 months. When we graph out the profit to unit sold chart, we see the famous J-Curve:

There is a very important distinction here because this nets out a new cash flow deficit beyond that of the traditional R&D phase and fixed costs.

In the world of SaaS, the business is essentially financing the customer for better long term economics.

When we compare the pros and cons of SaaS vs traditional software businesses. The argument is that over time, the SaaS business should have better economics, however, the con is that we run into a short term liquidity problem for the business as they're essentially taken on the role of the financier.

We can see it here, where because the fundamental unit economics of the SaaS business is better their long term growth trajectory and acquisition engine is more profitable than the old model. However, that is at the expense of a capital deficit in the shorter term.

Result: founder loses

This dilemma poses a financing problem. Today, this role of capital requirement is filled by equity dollars of Venture Capital.

If you take a step back and think about it. The customer wins, because the nature of SaaS is that the value a customer derives from a product is being financed by the business. The VC wins, because they now have a new breed of companies that all need their capital to scale and grow.

The business however is better in the long run because they are building a more profitable business with stronger unit economics.

However, in this situation, the founder loses... as they suffer heavily dilutions in order to finance that growth gap.

Today's financing thesis is suboptimal

The current financing thesis as dictated by the market is: "equity capital is the most risk-adjusted form of financing the growth of a SaaS business".

However, is that really the case? Likely not. Equity capital is a very catch-all financing solution.

There is likely an opportunity for a new entrant to finance the gap between LTV and CAC that's better risk-adjusted than equity capital.

We're already starting to see this shift of non-equity capital that's coming to the traditional space of Venture Capital, this is going to greatly compress VC returns. As they've largely benefited from this surge of SaaS models and founders needing to over dilute themselves.

As we shift more towards a “buying customers to realize their future LTV”, this holds true for all business types. As a business model gets more mature and we better understand each business model’s risk profile, we should be able to better underwrite them as well with more favourable solutions.

For further reading, I really like this article by Alex Danco, it has a lot of the exact same points and great links and drives more in-depth on the history than I have here.